Corporate Transparency Act Disclosure of Beneficial Ownership Information Impact on Non-U.S. Residents

The Corporate Transparency Act (CTA) is a new federal law requiring most domestic and foreign business entities formed or registered to do business in the United States to disclose information about their beneficial owners to the Financial Crimes Enforcement Network (FinCEN).

Update April 19: You can now officially use your registered agent’s or virtual address as your company’s address on the BOI report. Ensure you get permission first from your registered agent or use their virtual address for FinCEN. Check out the updated FAQ F.12 on FinCEN’s website at this link.

Update March 7: Here is a win for NSBA members; they won a lawsuit against the CTA, and now their members do not need to file a BOI report! See details here: https://www.nsba.biz/post/press-judge-rules-in-favor-of-nsba-in-lawsuit-over-corporate-transparency-act. Will this ruling last? Not likely. Once the case enters the appeal process, it will likely be escalated to the Supreme Court, where the lower court’s decision may be reversed. Therefore, this may only serve as a temporary setback to filing a BOI report unless, by some chance, the Supreme Court deems the CTA unconstitutional.

Update March 1: A new challenge for non-residents with a U.S. company is how to fill out the BOI report for the U.S. business address. For most U.S. entities formed by non-residents, the single-member LLC disregarded is the most popular; either use a registered agent address on the filed articles and with the IRS or a virtual address for both. Unfortunately, on the BOI report, they will not accept either address. The BOI report says the reporting company address: the reporting address, which is the address where the company does “business,” should be a physical US address; registered agent, virtual office, and PO box are not accepted. This has changed in April. See the updated FAQ at this link.

The street address should be the principal place of business. Otherwise, it should be the primary location in the United States or U.S. Territory where the reporting company conducts business. See items 11-15 at https://boiefiling.fincen.gov/resources/BOIR_Filing_Instructions.pdf.

In summary, the rule says to report the address of the principal place of business in the United States or, if the reporting company’s principal place of business is not in the United States, the primary location in the United States where the company conducts business.

Remember, the BOI report information is shared with the IRS, so plan and consult with a professional to determine which U.S. address you will use as your principal place of conducting business in the U.S.

Update: The BOI report is open and available to complete for all entities filed before 2024 and for new filings in 2024 (Jan. 2024). Go to this link to file. For new entities filed in 2024, you will need the company applicant’s FinCEN identifier.

Update: Alert: FinCEN has been notified of recent fraudulent attempts to solicit information from individuals and entities who may be subject to reporting requirements under the Corporate Transparency Act (Nov. 2023). The fraudulent correspondence may be titled “Important Compliance Notice” and asks the recipient to click on a URL or to scan a QR code. Those e-mails or letters are fraudulent. FinCEN does not send unsolicited requests. Please do not respond to these fraudulent messages, click on any links, or scan any QR codes within them.

You may receive notifications from companies or firms that will provide a service to file your beneficial owner’s information (BOI) report on your behalf for a fee. That is acceptable and very different from a company that uses marketing to appear as a government-type agency, even though they may have a disclaimer in fine print at the bottom.

These companies are not affiliated with the government and may charge excessive service fees. If you decide to use a third-party service to file your BOI report, it is important to be aware of these differences and choose a reputable company.

It’s important to note that while the initial filing of beneficial ownership information with FinCEN under the Corporate Transparency Act is a one-time requirement in 2024, the real significance lies in the obligation to update this information whenever changes occur. Failing to update this information could lead to fines.

Think about how often you’ve moved or established new businesses. If you have any role in managing or controlling these entities and haven’t kept track of these changes, you could be subject to compliance penalties. It’s essential to thoroughly understand these regulations and ensure that all entities under your control comply with 2024 onwards.

Here is what you need to know.

The CTA is now in effect as of January 1, 2024. The guidelines for filling out your beneficial owner’s statement are now available online at this link.

How will this impact U.S. and non-U.S. resident e-commerce sellers and other agencies selling through a U.S. LLC?

Before we get to that, let’s address what happened with disclosing ownership before this change:

Before the Corporate Transparency Act (CTA), U.S. residents were not required to disclose their ownership of 25% or more of a U.S. entity to any government agency. However, several other laws and regulations may require U.S. residents to disclose their ownership of U.S. entities, such as:

The Bank Secrecy Act (BSA): The BSA requires certain financial institutions to report suspicious activity to the Financial Crimes Enforcement Network (FinCEN). If a financial institution suspects that a customer is using its services to launder money or commit other financial crimes, it may be required to file a Suspicious Activity Report (SAR) with FinCEN. SARs can include information about the customer’s identity, ownership of U.S. entities, and financial transactions.

The Foreign Account Tax Compliance Act (FATCA): FATCA requires certain U.S. residents and citizens with foreign financial accounts to report those accounts to the Internal Revenue Service (IRS). If a U.S. resident owns 25% or more of a foreign entity, that entity may be considered a foreign financial account.

The Controlled Foreign Corporations (CFC) provisions of the Internal Revenue Code: The CFC provisions tax U.S. shareholders on the undistributed earnings of their CFCs, which are foreign corporations controlled by U.S. persons. If a U.S. resident owns 25% or more of a foreign entity, that entity may be considered a CFC.

In addition to these laws and regulations, depending on the type of entity and the jurisdiction in which it is formed, U.S. residents may also be required to disclose their ownership of U.S. entities to state and local government agencies.

The CTA will change the landscape for disclosure of ownership of U.S. entities by requiring most domestic reporting companies to file reports disclosing their beneficial owners and company applicants with FinCEN.

What is a beneficial owner?

A beneficial owner is an individual who exercises substantial control over an entity, either directly or indirectly, or who owns or controls 25%or more of the entity’s equity interests.

According to FinCEN’s BOI Small Compliance Guide – see at this link, your company can identify beneficial owners by taking the following steps:

Step 1: Identify individuals who exercise substantial control over the company. Examples are provided below to help you identify those individuals.

Step 2: Identify the types of ownership interests in your company and the individuals that hold those ownership interests. Examples are provided below to help with identification.

Step 3: Calculate the percentage of ownership interests held directly or indirectly by individuals to identify individuals who own or control, directly or indirectly, at least 25 percent of the ownership interests of the company.

How do you determine who has substantial control over a company? Here are the questions to ask provided by FinCEN’s BOI Small Compliance Guide (see page 26).

1. Does your company have a president, chief financial officer, general counsel, chief executive officer, or chief operating officer?

2. Does your company have any other officers that perform functions similar to those of a President, chief financial officer, general counsel, chief executive officer, or chief operating officer? Note: One individual may perform one or more functions for a company, or a company may not have an individual who performs any of these functions. These are senior officers in your company.

3. Does your company have a board of directors or similar body, AND does any individual have the ability to appoint or remove a majority of that board or body?

4. Does any individual have the ability to appoint or remove a senior officer of your company? Questions 3 and 4 are individuals with appointment or removal authority over your company.

5. Does any individual direct, determine, or have substantial influence over important decisions made by your company, including decisions regarding your company’s business, finances, or structure? These are important decision-makers in your company.

Note: Certain employees who might fit this description are exempt from the beneficial owner definition. See section 2.4 of the guide for more information.

6. Are there other individuals who have substantial control over your company in ways other than those identified in 1-5 above? These are individuals to whom the catch-all would apply.

What entities are covered by the Corporate Transparency Act? Which are Exempt?

The CTA covers most domestic and foreign business entities formed or registered to do business in the United States, including corporations, limited liability companies (LLCs), partnerships, and trusts. Exemptions are provided for certain entities, such as publicly traded companies, banks, and investment funds. “Large operating companies” are also exempt, which are entities that (i) have more than 20 full-time U.S. employees (not counting employees of affiliated entities), (ii) reported more than $5 million of revenue from U.S. sources on a consolidated basis to the IRS for the previous year and (iii) have an operating presence at a physical location in the United States.

Overall, there are 23 exempt categories, and your first step is to determine if you have a reporting requirement.

The big category is #23, called “Inactive entity.” What does that mean?

Here is what FinCEN says about an inactive entity qualification:

An entity qualifies for the inactive entity exemption if all six of the following criteria apply:

(1) The entity was in existence on or before January 1, 2020.

(2) The entity is not engaged in active business.

(3) The entity is not owned by a foreign person, whether directly or indirectly, wholly or partially. “Foreign person” means a person who is not a United States person. A United States person is defined in section 7701(a)(30) of the Internal Revenue Code of 1986 as a citizen or resident of the United States, domestic partnership and corporation, and other estates and trusts.

(4) The entity has not experienced any change in ownership in the preceding twelve-month period.

(5) The entity has not sent or received any funds in an amount greater than $1,000, either directly or through any financial account in which the entity or any affiliate of the entity had an interest, in the preceding twelve-month period.

(6) The entity does not otherwise hold any kind or type of assets, whether in the United States or abroad, including any ownership interest in any corporation, limited liability company, or other similar entity.

FinCEN’s Small Entity Compliance Guideincludes checklists for this exemption (see exemption #23) and for the additional exemptions to the reporting requirements (see Chapter 1.2, “Is my company exempt from the reporting requirements?”).

Is the reporting requirement applicable to foreign companies registered for business operations in the U.S.?

It is important to note that the Corporate Transparency Act applies to domestic and foreign companies registered to do business in a U.S. state. While foreign registration was previously required in some states to obtain a sales tax permit, this requirement has been eliminated in most cases.

However, the Corporate Transparency Act now requires all companies registered to do business in a U.S. state to disclose their beneficial ownership information, regardless of their origin.

Additionally, in the past, some states, such as Florida, required foreign entities to register with the secretary of state before opening a U.S. bank account.

What information must be disclosed?

Entities covered by the CTA must disclose the following information about their beneficial owners to FinCEN:

Full name

Date of birth

Address

Social Security number or taxpayer identification number

If you don’t want to give your SSN as the owner, don’t be the owner. What if another entity is the owner?

Does that mean you provide the EIN? Probably, but what about the second entity, who is the owner? What if you own that entity? Doesn’t that mean you would provide your SSN (assuming you have one) for the second entity? Yes.

Does that help at all? It might depend upon the nature of the company, and keep in mind the 23 exemptions, of which one is whether you have 20 or more employees or report over $5 million in revenues.

What about non-residents who do not have an SSN or a TIN (taxpayer identification number)?

The ITIN is the most common for non-residents. What does that trigger regarding your U.S. filing responsibilities, and how do you even obtain an ITIN if you don’t have a U.S. filing requirement?

At NCP, our CEO, Scott Letourneau, is a certified tax advisor, consults often on these and other subjects, and works with a mastermind group of tax attorneys and other legal professionals for support. Learn more at this link.

How will the CTA impact new entity formations?

The CTA will add a new step to the new entity formation process. Entities formed or registered to do business in the United States on or after January 1, 2024, must file a report with FinCEN disclosing information about their beneficial owners within 30 days of formation or registration. If you have active entities with the secretary of state but are not active for any business or holding assets, it would be best to clean them up and dissolve them before January 1st, 2024.

But on Sept. 28, 2023, FinCEN proposed extending this deadline to 90 days for entities formed in 2024.

After the initial report, there is no annual or quarterly filing requirement. However, reporting companies must file an amendment within 30 days after any change to their reported information.

Entities already formed or registered to do business in the United States on January 1, 2024, will have until January 1, 2025, to file a report with FinCEN disclosing information about their beneficial owners.

New Entity Strategy: If you are starting a new business entity in January 2024, it is best to file the entity formation documents before January 1st, and when applying for the EIN (Employer Identification Number) through Form SS-4, use a start date of January 1st, 2024. This will give you the full 12 months to file your beneficial owner form instead of only 90 days in 2024.

What are the consequences of failing to comply with the CTA?

Entities that fail to comply with the CTA’s reporting requirements may be subject to civil penalties of up to $500 per day. Individuals who knowingly and willfully fail to comply with the CTA’s reporting requirements may be subject to criminal penalties of up to five years in prison and a fine of up to $250,000.

What should businesses do to prepare for the CTA?

Businesses should start preparing for the CTA by identifying their beneficial owners and gathering the required information about them. Businesses should also develop a plan for complying with the CTA’s reporting requirements.

The public will not have direct access to the beneficial ownership information reported due to the Corporate Transparency Act (CTA).

The CTA requires FinCEN to maintain the information in a secure, nonpublic database. However, FinCEN may disclose the information to law enforcement and other government agencies for authorized purposes.

FinCEN has not yet announced any plans to make beneficial ownership information available publicly. However, some experts believe that it is likely that FinCEN will eventually make the information publicly available, at least in a limited way. Even if no information is public, it goes to the IRS. We foresee where FinCEN will scrape the list of all entities that apply who are registered with the secretary of state and compare that to the list of companies that file with FinCEN by the end of 2024, and cross-reference with the IRS to go after companies in 2025, that are not in compliance. Your address will be important because it may have changed since you formed the LLC and obtained the EIN. So, you may never see the fine mailed directly to you due to an address change.

Non-residents need to be aware of a complete U.S. LLC formation strategy and the best address service that is detailed and reliable so they can stay in compliance with FinCEN. Remember, if you make any changes to your ownership of your LLC, the manager, the responsible party, or the owner’s home address…, you must update your account with FinCEN or face a potential civil penalty of up to $500 for each day that the violation continues, or criminal penalties, including imprisonment for up to two years and/or a fine of up to $10,000.

Will your Amazon brand competitors finally discover the “true owner” of the Amazon account?

Remember, on your Amazon account, your “brand name,” which is the same as your “display name,” will rarely have your LLC name. Your “sold by name,” also known as your “storefront name,” is separate. In the big picture, if your LLC name is not your “brand name,” it will be only the legal entity on your account and not show up on your Amazon page with your products.

Anyone can search the USPTO database to determine who owns a trademark. This includes trademarks owned by Amazon businesses, but the CTA is not expected to make beneficial ownership information public now.

Your privacy from other competitors should be safe. At the end of the day, most competitors don’t need to know who the owner is to compete; they need to know their competition. In litigation, privacy and asset discovery are much more important when looking for leverage to fast-track a case.

What about the IRS as a non-resident individual or company owning a U.S. LLC operating a U.S. business on Amazon?

That could be a real issue for many sellers who have taken a strong stance that they are not engaged in a U.S. trade or business and do not have any effectively connected income with that U.S. trade or business. Determining whether a seller is engaged in a U.S. trade or business is a complex process that requires carefully analyzing all relevant facts and circumstances.

Did you or your foreign company file a protective return? If not, perhaps now is the time before the IRS has all the ownership information.

Tax Form 5472 requires reporting corporations to disclose information about their 25% or more foreign shareholders to the IRS, and now the Corporate Transparency Act (CTA) will also require reporting companies to disclose information about their beneficial owners to the Financial Crimes Enforcement Network (FinCEN). FinCEN may then share this information with the IRS and other law enforcement agencies. The key for non-residents becomes what U.S. tax returns the owners file, if any. Remember, you may not have had any responsibility to file a return by the owner.

What sellers can do

Non-resident sellers who form a U.S. single-member LLC as a non-resident individual or a foreign corporation may want to consider filing a protective U.S. tax return.

There are a few benefits for U.S. LLCs owned by foreign companies to file a protective US tax return:

Preserve the right to deduct expenses. If a U.S. LLC owned by a foreign company does not file a tax return, it will lose the right to deduct any expenses incurred, even if those expenses are related to business activities that generate income in the United States. Filing a protective tax return preserves the right to deduct these expenses, even if no income is reported.

Establish a tax filing history. Filing a protective tax return for a U.S. LLC owned by a foreign company can help establish a tax filing history for the entity. This can be beneficial if the company later starts reporting income in the United States. A good tax filing history can make obtaining a U.S. tax identification number easier and opening bank accounts and other financial accounts in the United States.

Avoid penalties and interest. If a U.S. LLC owned by a foreign company fails to file a tax return, even if it has no income to report, it may be subject to penalties and interest. Filing a protective tax return can help to avoid these penalties and interest.

It is important to note that filing a protective tax return does not mean the U.S. LLC owned by a foreign company must pay taxes in the United States. The company will only be required to pay taxes if it has income effectively connected with a U.S. trade or business.

Here are some specific examples of how filing a protective tax return can benefit a U.S. LLC owned by a foreign company:

A U.S. LLC owned by a foreign company is engaged in limited business activities in the United States, such as maintaining a bank account and attending trade shows. The company does not earn income from these activities. However, it wants to preserve the right to deduct any expenses incurred with these activities. To do so, the company can file a protective tax return.

A U.S. LLC owned by a foreign company is starting a new business there. The company does not expect any income in the first year of operation. However, it wants to establish a tax filing history and avoid penalties and interest. To achieve these goals, the company can file a protective tax return.

A U.S. LLC owned by a foreign company has been inactive for several years. The company now wants to start reporting income in the United States. The company can file a protective tax return to re-establish its tax filing history and avoid penalties and interest.

If you are considering filing a protective tax return for a U.S. LLC owned by a foreign company, you should consult a tax advisor to ensure you comply with all US tax laws.

Are all the owners disclosed?

The Corporate Transparency Act (CTA) requires reporting companies to identify all beneficial owners, regardless of ownership percentage. A beneficial owner is an individual who exercises substantial control over an entity, either directly or indirectly, or who owns or controls 25% or more of the entity’s equity interests.

This means that reporting companies must identify all individuals who meet any of the following criteria:

They are a senior officer of the entity.

They have authority over the entity’s management or finances.

They have the ability to make important decisions about the entity’s business.

They have a significant financial interest in the entity.

Reporting companies must also identify any individual who controls one or more intermediary entities that control the reporting company.

The CTA does not provide a specific definition of “substantial control.” However, FinCEN has issued guidance that provides some examples of activities that may constitute substantial control. These activities include:

Appointing or removing senior officers of the entity.

Approving major transactions or investments.

Setting the entity’s budget or financial goals.

Approving the entity’s strategic plan.

Having the ability to veto important decisions made by the entity.

Reporting companies must file a report with FinCEN identifying their beneficial owners within 30 days of formation or registration (but 90 days for those entities formed in 2024). The report must include the following information for each beneficial owner:

Full name

Date of birth

Address

Social Security number or taxpayer identification number (TIN). Don’t want to disclose your SSN as a U.S. resident? What about a non-resident entity registered to do business in the U.S.? Here is what FinCEN advises: If a foreign reporting company has not been issued a TIN, report a tax identification number issued by a foreign jurisdiction and the name of such jurisdiction.

If the beneficial owner is a foreign individual, the reporting company must also provide the beneficial owner’s passport number and country of citizenship.

The CTA is a significant new law requiring reporting companies to disclose more information about their beneficial owners. FinCEN and other law enforcement agencies will use this information to investigate and prevent financial crimes.

Are there other areas where U.S. residents must disclose their ownership in a U.S. entity formation?

Schedule G of Form 1120 requires corporations to disclose ownership details of any individual or entity that owns, directly or indirectly, 20% or more of the corporation’s voting stock. The IRS uses this information to identify and track large shareholders of corporations.

Schedule G requires corporations to report the following information about their large shareholders:

Name

Taxpayer identification number (TIN)

Country of citizenship

Percentage of voting stock owned

Corporations must also report any changes in ownership of 20% or more of their voting stock to the IRS within 30 days of the change.

The ownership disclosure requirements on Schedule G are different from the CTA’s reporting requirements in a few key ways:

Schedule G only applies to large shareholders who own 20% or more of a corporation’s voting stock, while the CTA applies to all beneficial owners of domestic reporting companies.

Schedule G only applies to U.S. corporations, while the CTA applies to both U.S. and foreign reporting companies.

Schedule G is filed with the IRS, while the CTA report is filed with FinCEN.

Despite these differences, Schedule G and the CTA are important tools for the IRS and FinCEN to combat money laundering, terrorist financing, and other financial crimes.

If you file Form 2553 to make the S election, you must disclose each shareholder’s ownership percentage. This information is reported in Part I of Form 2553.

In addition to disclosing each shareholder’s ownership percentage, you must also obtain the consent of all shareholders who own stock on the date the election is filed. This consent is obtained by having each shareholder sign the Shareholder’s Consent Statement in Part I of Form 2553.

The ownership disclosure requirements on Form 2553 are similar to those on Schedule G of Form 1120. However, there are a few key differences:

Form 2553 requires disclosure of the ownership percentage of all shareholders, regardless of whether they own 20% or more of the corporation’s stock.

Form 2553 requires the consent of all shareholders who own stock on the date the election is filed.

Form 2553 is filed with the IRS while you file your corporation’s federal income tax return.

The ownership disclosure requirements on Form 2553 are important for the IRS to administer the S corporation election. The IRS uses this information to ensure that all shareholders know and consent to the election.

Conclusion

The Corporate Transparency Act is a significant new law that will significantly impact new entity formations for U.S. and non-U.S. residents. Businesses should start preparing for the CTA by identifying their beneficial owners and gathering the required information about them. Businesses should also develop a plan for complying with the CTA’s reporting requirements.

Remember, existing entities required to report have until the end of 2024 to submit their filings. It’s important to note that any updates or clarifications to the instructions or guidelines will likely occur within the first 30-60 days of the new year. Therefore, delaying your report submissions for a few months can be strategic.

U.S. Bank Compliance with LLC Formations: An Essential Guide

Navigating the complexity of U.S. tax and legal compliance can often seem like a formidable challenge, particularly when it involves a single-member LLC disregarded to expand your U.S. e-commerce business to the U.S. You will now realize that a U.S. single-member LLC disregarded is NOT your best option when doing business in the U.S., not only from a banking point of view but also from changing the legal entity on your existing Amazon seller account.

A Major Update: A wave of transformation has recently swept over the requirements for financial technology companies interacting with U.S. banks. A pivotal aspect of this transformation is the stipulation for applicants to be recognized as a “U.S. person” to avail of their services. Traditional banks, such as Wells Fargo, Bank of America, Chase, and Citibank, want your U.S. company to have a U.S. office with a lease agreement or utility bill (not a business phone in most cases). The banks want to work with people from the U.S. who are doing the work. As you can imagine, this directly conflicts with your U.S. taxation goals as a non-resident. Experienced consulting is recommended to navigate this constantly moving target. Even traveling to the U.S. to open a personal bank account with the major banks is much more different in 2024 than before. Banks want to work with resident aliens who live in the U.S. with an apartment or residential address and utility bill in their personal name to match.

One of these regulations is the Foreign Account Tax Compliance Act (FATCA), which requires U.S. banks to report certain information about their foreign account holders to the IRS. To comply with FATCA, many banks must collect and report information about their account holders, including their tax residency status.

Another regulation that banks must comply with is the Bank Secrecy Act (BSA), which requires U.S. banks to identify and report suspicious activity. To comply with the BSA, banks must collect and verify the identity of all its account holders.

By requiring non-resident customers to be U.S. taxpayers, banks can ensure they can comply with FATCA and the BSA.

This poses a critical question: What does this change mean for entities like yours?

Defining the ‘U.S. Person’ from an Entity Perspective:

Corporations and partnerships are orchestrated under the umbrella of U.S. state law.

Trusts that resonate with the “U.S. court” and “U.S. control” criteria, irrespective of their legal domicile.

Estates that resonate with a nuanced “facts and circumstances” examination involve considerations like the executor’s residence and the predominant location of assets.

For non-residents owning a single-member disregarded LLC, it’s essential to realize that such an entity typically does not align with the qualifications of a U.S. taxpayer.

Entities that Walk the U.S. Person Pathway for Non-Residents:

A U.S. LLC navigated through the tax landscape as a partnership (of course, this involves a partnership, which may be an existing entity from your home country, assuming not a single-member LLC that is disregarded and owned by the same owner).

A U.S. LLC taxed as a corporation (this selection creates another issue if you have a need for a U.S. ITIN, but we have solutions).

The journey becomes particularly tumultuous when entities are called upon to affirm their U.S. person status while engaging with U.S. technology giants like Mercury. This is similar to completing a W-9, and under part 2, it says, under penalty of perjury, that you certify several items, including that you are a U.S. person.

Cautionary Winds: You do not want to perjury yourself on an IRS form or anything related close to that with U.S. banking. The fines and penalties can be severe. Other online banks that do not yet have these requirements may soon follow this trend, so make sure you are prepared for the best options for your U.S. e-commerce business, banking, and the overall tax results supporting your business growth.

Navigating Toward Solutions:

At NCP, we are here to guide you as you grow your business in the U.S. We will help you with many things like choosing the best banking options for now and the future, meeting Amazon’s insurance rules, setting up your U.S. business correctly, and understanding what taxes you will need to pay. We will also help you update your Amazon seller account to avoid extra checks like showing more utility bills. We make it easier for you to expand your business in the U.S.

If you need additional support in converting your existing single-member LLC disregarded to a corporation or partnership and retaking the Amazon tax interview, or perhaps you want to expand with the best options for your situation, we are here to help. Book a call with our team to clarify our best options and support.

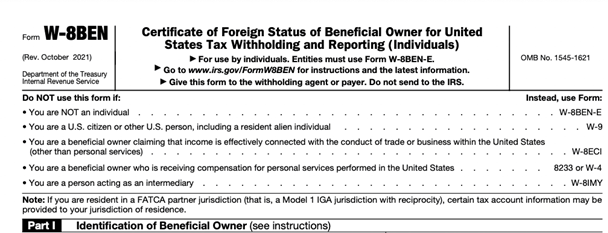

Decoding the W-8BEN: Does It Really Shield You from U.S. Taxes?

E-commerce is booming, as are the complexities of navigating U.S. tax regulations! This is a must-read if you’re an e-commerce seller, particularly one that deals with major platforms like Amazon. Need help with the tax interview required by the marketplaces? Are you exempt from U.S. taxes? Dive in!

W-8BEN or W-8ECI? Understanding the Nuances

Marketplaces might offer you a W-8BEN form, but does that mean you’re safe from Uncle Sam’s tax net? Nope.

Forms Unraveled: If you’re only given a Form W-8BEN or its variants, it could imply your earnings are seen as FDAP income. But this isn’t the full story.

Beyond the Marketplace: Despite your business on a platform, you can have a U.S. Trade or Business (USTOB) and Effectively Connected Income (ECI) that the marketplace knows nothing about.

Tax Reporting: A marketplace not issuing a Form 1042-S because of the W-8BEN doesn’t give you a free pass. If you’ve got USTOB and ECI, a tax return awaits you! Amazon sellers, take note: just because Amazon hands you a W-8BEN doesn’t mean you’re free from USTOB or ECI.

Why Partner with NCP?

Expertise: With the intricacies of U.S. tax codes, wouldn’t you prefer an expert by your side? Enter NCP.

Tailored Tax Consultation: We don’t believe in one-size-fits-all. We craft our tax advice based on your unique circumstances as a non-resident seller.

Form a U.S. Entity with Ease: With our guidance, set up your U.S. single-member LLC disregarded entity without breaking a sweat.

Stay Compliant, Stay Informed: With regulations constantly changing, our dedicated team ensures you’re always ahead of the curve.

E-commerce Bonus: Special compliance offerings for Amazon, Walmart, Shopify sellers, and beyond!

In collaboration with expert U.S. tax attorneys and CPAs, our team is here to help you sail through the turbulent waters of U.S. tax regulations. Your business growth is our mission.

Let NCP Be Your Tax Beacon – You deserve nothing but the best when it comes to launching your U.S. business. Dive deeper into the world of U.S. taxes with us. Your success story is just a consultation away!

Shopify Payments U.S. for Non-Resident Sellers: A Step-by-Step Guide

As an existing non-resident Shopify seller, you likely started your Shopify store with Shopify payments linked to your region.

However, if you’d like to set up a Shopify Payments account for a region different from your location, such as the U.S., you can submit your case to the Shopify Support Team and follow the steps below.

Not Everyone Will Qualify for Shopify Payments (Even If You Meet All the Steps)

However, having the requested documents does not guarantee that you’ll be approved for Shopify Payments. Shopify’s internal specialist teams will ultimately make the call regarding supportability.

What is Required to Qualify for Shopify Payments?

A business must have physical operations on US soil to use Shopify Payments US. A USD checking account is also needed, opened with a US banking institution and located on US soil. Virtual banks and currency services will not work for this, as it has to be an actual US bank.

Items you will need to be ELIGIBLE for Shopify Payments U.S.

US Tax ID: To get a Shopify Payments US account, you’ll need a US tax identification number (TIN). If you’re a business like an LLC or Corporation, you need an Employer Identification Number (EIN). You’ll need a Social Security Number (SSN) if you’re a Sole Proprietor.

Physical Operations in the US: A US tax ID isn’t enough. Your business needs to have a physical presence in the United States. This means having a real operation there. A lease agreement is required (which we do provide) as part of our virtual address service with our U.S. entities.

Specifically, here is what Shopify says about this part to qualify for Shopify Payments: In order to be eligible for Shopify payments in a particular region, you must EITHER (a) be PHYSICALLY present within that region (not 99% of you as non-residents), OR (b), have an OPERATIONAL presence with that region.

To establish PHYSICAL PRESENCE, they will require a document in your name (personal name) such as a utility bill (e.g., water, electricity, or gas bill from the past three months (not cell phone), PERSONAL LEASE AGREEMENT (dated) OR property insurance (dated).

By the way, this is the same evaluation in 2024 for local banks in the U.S. for a personal bank account (which has changed in the last two years); they want you to lease an apartment in your own name and have one major utility bill in your own name with that address.

If you are NOT physically present within the region selected, we would INSTEAD need to establish an OPERATIONAL PRESENCE. This can be done, for example, by showing you have RENTED or OWNED warehouse space or retail space in the U.S. For example, see warehouse space for sale in Las Vegas at this link. Here is warehouse space for rent in Las Vegas at this link.

Please note (from Shopify) that registering a company within a region is NOT sufficient to establish an operational presence. Translation: a cheap online LLC with an EIN and address will not qualify you for Shopify payments in the U.S.

Government-Issued Photo ID: You’ll need a government-issued ID with your photo on it (like a driver’s license or passport) for verification. Sometimes, they might accept non-US IDs, but it’s best to check with Shopify.

Business Registration Document: Ensure your business is officially registered in the US. This proves that your business is legitimate. The key is, are you creating a U.S. person? And you need to be clear on the U.S. tax responsibilities that it creates.

Proof of US Operation: You must show evidence that your business operates from the US. A bank statement or forwarding service won’t work as proof. It would be best if you had something more reliable. A utility bill and lease agreement is recommended.

USD Checking Account: You’ll need a real US bank account in US dollars to handle transactions. Virtual banks or currency services won’t be accepted.

SSN or ITIN Verification

U.S. merchants enjoy the convenience of Shopify Payments, but there are specific requirements they must meet to use the U.S. version of this payment gateway. Let’s explore the obligations of U.S. merchants:

U.S. merchants setting up a Shopify Payments US account must provide all nine digits of their Social Security Number (SSN) or Individual Taxpayer Identification Number (ITIN) for verification purposes. This is a mandatory step, even if the merchant already has an Employer Identification Number (EIN) for their business.

This rule still applies even if you have an EIN for your business. Shopify needs to bypass this step on sign-up. To learn more about this, refer to the US Shopify Payment Terms of Service: Section B-3.

Meeting this requirement helps Shopify ensure the merchant is a legitimate entity operating in the U.S. and adheres to relevant regulations and tax laws.

Processing Time for ITIN

In situations where obtaining an ITIN is necessary, it’s important to consider the potential impact on your LLC’s setup in the short and long term. Processing an ITIN application can take time, typically extending to 3-4 months. Therefore, planning accordingly and anticipating delays during this process is essential.

Possible Exemptions for ITIN

In some cases, Shopify may waive the requirement for an ITIN based on the account holder’s unique circumstances. Each case is reviewed individually, and exemptions are considered on a case-by-case basis. If Shopify determines that the account holder’s circumstances warrant an exemption, they may proceed without an ITIN.

Considerations for Setting up the LLC

When setting up your LLC, it’s essential to consider the potential need for an ITIN, especially if you plan to use Shopify Payments as your payment gateway. This consideration becomes even more critical if you use your LLC as the legal entity for insurance purposes on platforms like Amazon.

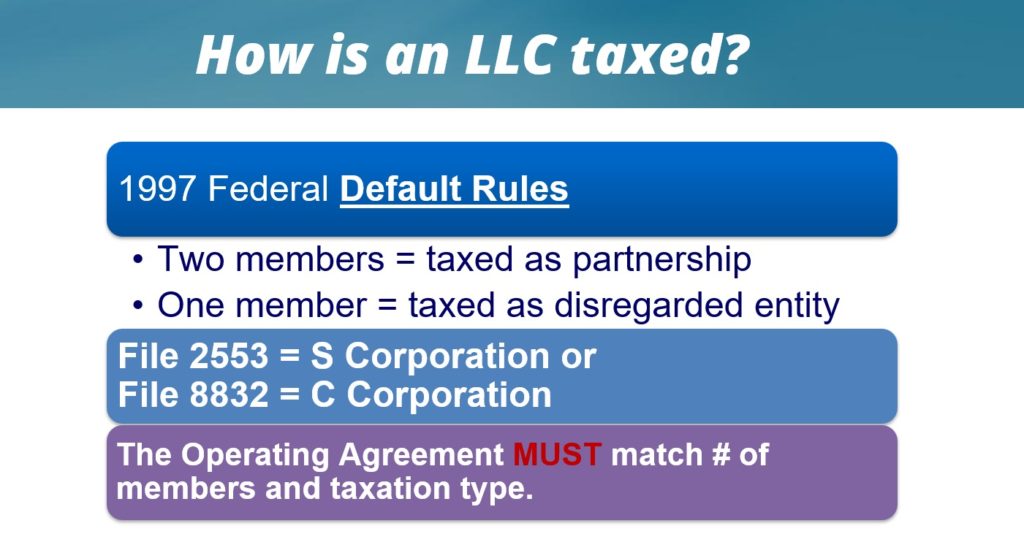

An LLC in the U.S. can be taxed in four different ways, and only three apply to most non-residents: an LLC disregarded for tax purposes, an LLC taxed as a corporation, or an LLC taxed as a partnership. The only option to obtain an ITIN with the LLC is an LLC that is disregarded for tax purposes, and an ITIN is usually only available when personal U.S. taxes are due on a 1040NR tax return. When you form an LLC, how it is managed and a complete formation with formalities to protect your U.S. business is key. Completing a W-9 means you are creating a U.S. person for tax purposes.

Another key is understanding your full U.S. tax responsibilities when you form a single-member LLC that is disregarded to determine if the LLC or owner is engaged in a U.S. trade or business and has effectively connected income.

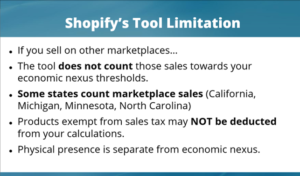

Separately, it is the responsibility of sales tax compliance. Only turn on sales tax settings in all states by knowing the tax rules and being licensed in each state where you have crossed nexus thresholds or have physical nexus.

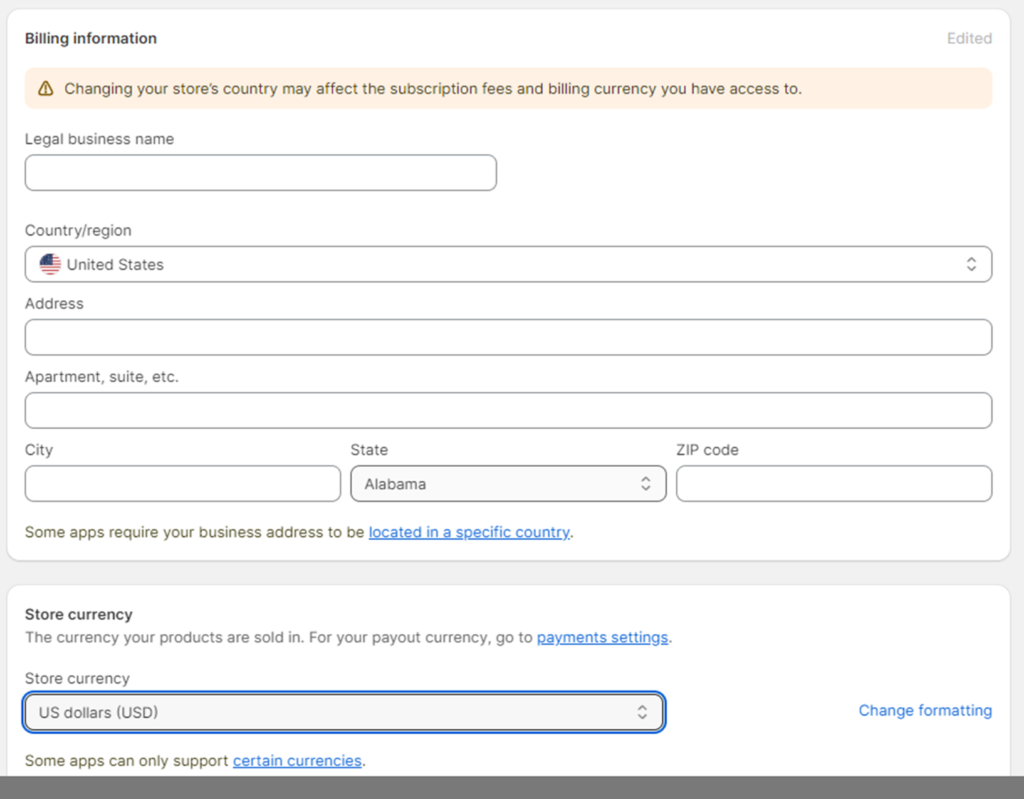

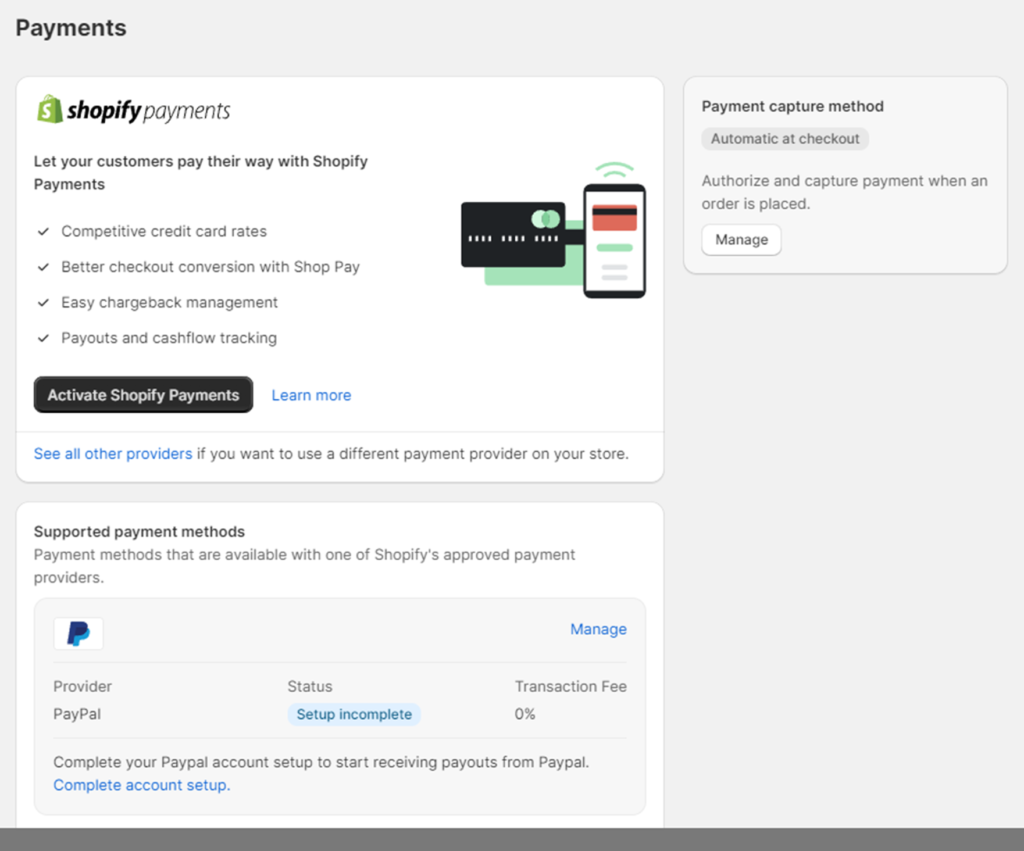

How to Update Your Shopify Store to Qualify for Shopify Payments U.S.

You can change your address to a US location. Access your dashboard and click the “Settings” option to get started. If you go to “Payments, “you will see the option to activate the Shopify payment gateway.

Once you’ve successfully established your US company, whether a US citizen or a non-US citizen, the next step is to activate your Shopify payment gateway using the information obtained during your LLC formation.

Before activating, update your store address to the US address in your LLC documents. This US address can be utilized for your business or online applications.

During the Shopify payments activation process, you may encounter a field requesting your SSN’s last four (4) digits. In this case, you can replace it with the last four (4) digits of your ITIN.

Complete the remaining personal details as required, submit the information, and the Shopify review team soon notify you to determine if your application has been approved or if additional information is required.

———————–

Shopify’s verification takes place by activating the Shopify Payments account.

The instruction says to change or update the store address to a US address but doesn’t ask for any verification.

The next step is to activate Shopify Payments. You would only need to provide entity documents to activate Shopify Payments.

If applicable, you can enter your Business Number or Tax Identification Number depending on which country your business is located in. They will ask the following:

Business Type

Individual/Sole Proprietorship – need SSN/ITIN or SIN – Social Insurance Number (for Canada)

Corporation

Nonprofit

Partnership

Business Number/TIN

Business Address

Personal Details

First and Last Name

DOB

Product Details

Customer Billing Statement

Banking Information

If your store is in Europe, you must provide a VAT number or indicate that you don’t have one.

If you set up your Shopify Payments account as a Corporation or LLC, you will still need to provide the name and date of birth of someone associated with the business. This is a requirement for verification purposes.

All businesses must submit a tax ID and are responsible for collecting and remitting tax on their sales.

You may also need to submit details about you and your business. This information is used to help identify merchants using Shopify Payments and is a requirement to comply with the terms of service.

What is required may differ from country to country. Typically, this includes:

documentation about the business associated with the Shopify Payments account

owner of the business

or an individual with signing authority for the business.

If Shopify is unable to verify your identity using the information above, you may be asked to submit additional documentation that could include the following:

Proof of identity

Proof of home address

or, Proof of business verification

If your business can’t be verified using the information you provided at the time of Shopify Payments sign-up, additional documentation might be requested. Just so you know, the documents that you provide must include the business name, business address, and company registration number or VAT number.

For business verification, upload your official federal business registration document, including your federal tax registration number, if available.

Business documents require the following:

Documents must be clear and large enough to read.

Documents must be valid and representative of up-to-date registration.

Complete documents must be uploaded. A complete document contains the following:

The full business name, business address, and either VAT number OR company registration number are clearly stated and legible.

All pages of a multiple-page document. Upload a PDF containing all the relevant pages.

Documents can be uploaded in .png, .jpg, or .pdf format.

To help the verification process, when providing documents as evidence, ensure that your documentation:

is clear and large enough to read

is correct, valid, and up-to-date

is complete with all details visible

is free of any errors or typos

matches the information provided

Your identity, home address, and proof of entity documents must be reviewed and matched successfully to the information on your Shopify Payments account before your business can be fully verified.

Reviews of your Shopify Payments account can take up to 3 business days to complete.

Important: You must complete your Shopify Payments account setup, including all your business details and banking information, within 21 days of your first sale. If your account isn’t set up within 21 days, then payments might be automatically refunded to the customer.

For merchants in the European Union and Hong Kong, you need to complete the setup of your Shopify Payments account before you can accept payments from customers.

The first step is to schedule a strategy call to determine the U.S. LLC structure, ownership, and U.S. taxation for your situation. Learn more at this link.

Understanding Amazon’s Tax Interview: Key Mistakes Non-Residents Should Avoid with LLCs

Navigating Amazon’s tax interview for non-residents with U.S. LLC can be complicated, particularly regarding tax compliance. Many non-residents choose to operate as individuals or entities from their home country and will complete the W-8BEN or W-8BEN-E form during the Amazon tax interview.

Forming a U.S. single-member LLC often becomes necessary, especially in dropshipping scenarios where U.S. suppliers require dealing with U.S. companies (tip: don’t form your LLC in Wyoming when dropshipping). It might also be essential for securing U.S. insurance coverage when options are scarce in the non-resident’s country since many insurers do not provide services for non-residents in most countries. The necessity for insurance compliance increased after September 2021, particularly for sellers recording over $10,000 a month in sales.

It’s crucial to understand that U.S. suppliers may be indifferent about your Amazon sales, the proper completion of your Amazon tax interview, or even whether you’ve mistakenly committed tax fraud. However, insurance underwriters need to be more indifferent regarding claim filing.

Imagine this: Your insurance adjuster denies your claim because your U.S. LLC wasn’t genuinely managing your Amazon business or due to an ‘inadvertent trick’ played on the Amazon tax interview. Depending on the size of your claim, the repercussions can range from mildly inconvenient to severe. A $5K claim on a $1M policy might not raise eyebrows, but a claim worth $800K is likely to trigger intensive scrutiny from insurance company attorneys.

Suppose you’re an Amazon seller ticking the insurance box to get verified and are not concerned about coverage because you’re selling low-risk items like rubber kitchen spatulas. In that case, the above doesn’t apply. However, the looming risk of an Amazon suspension should pique your interest, so please keep reading.

Establishing a compliant U.S. LLC and meticulously navigating the Amazon tax interview are not just administrative formalities. An Amazon account will often not be verified, and you will be asked to provide additional verification in the form of a business utility bill linked to your U.S. address. That makes your verification process 10X more difficult. It is best to work with NCP and utilize our Amazon New Account 32-page Guide, or if you have already formed an LLC, book a consult with our CEO, Scott Letourneau, to review what you need to amend on your filing and changes to your Amazon account to help get your account verified.

Amazon Tax Interview Questions

Here are two pivotal questions you need to answer: Are you classified as an individual or a business for tax purposes? I think your response to this will change your question.

Upon selecting ‘individual,’ a critical note is displayed: if you choose this category, it will lead to the following question: Are you a U.S. citizen, a U.S. permanent resident (green card holder), or another type of U.S. resident alien? It’s worth noting that this question underwent revision in the Fall of 2022 to enhance clarity in the tax interview process.

The clarification under the initial question specifies that ‘individual’ encompasses sole proprietors or single-member LLCs where the owner is an individual.

For non-residents possessing a single-member LLC disregarded for tax reasons, the default choice is ‘individual.

Your Amazon “Sold By” Name

Consider this perspective on the Amazon storefront process: if your goal is to open an Amazon store using a disregarded LLC that you own, your LLC name can be the “store name,” but most often, your brand name will be your “store name” which will show as “sold by.”

The displayed ‘sold by’ name on your storefront does not want to be your personal name, which may not project the most enticing marketing image. This is because operating under an individual name might suggest that you need to generate more profit to form a tax-saving entity.

This message may resonate poorly with U.S. consumers. True, not all Amazon shoppers pay attention to the ‘sold by’ name. However, an increasing number of consumers are becoming aware that not all products are sold directly by Amazon, and they’re likely to take note of your brand name.

So, could you think carefully about the image you want to project to your potential customers? Because when it comes to branding, every detail counts.

Which ‘Sold by’ Brand Impresses More?

Detailed Seller Information

Business Name: Best Products, LLC

Business Address:

10785 W. Twain Ave. Ste. 229

Las Vegas, NV 89135

Or is this brand with all Chinese details?

Detailed Seller Information Business Name: HEFEI RUJU WANGLUOKEJI YOUXIANGONGSI Business Address: 蒙城北路2003号

骏杰嘉和大厦1001室

合肥市

庐阳区

安徽省

230041

CN

A U.S. consumer prefers a store brand that presents itself as U.S.-based, even while shopping on Amazon. While this factor might not directly reflect in your conversion tracking, it can undeniably influence sales outcomes. How can the ‘sold by’ name include an LLC?

There are two potential explanations: you completed the Amazon account setup correctly, separate from the tax interview, or the seller has manipulated the Amazon tax interview. This act carries its own set of troubles. You can read on this crucial topic for more information.

Amazon’s Reverification Under the INFORM Consumer Act

As we gear up for the INFORM Consumer Act’s enforcement on June 27, 2023, its impact on Amazon’s reverification process is indisputable. This consumer protection law aims to bolster online transparency, ensure fairness, and hold platforms accountable for their activities.

Update June 26th: We would like to inform you that starting July 7th, 2023, Amazon will initiate the withholding of funds for sellers who have not yet provided the required information necessary to comply with the INFORM Consumers Act.

Will Amazon take this deadline seriously? Yes.

Unliked the change in September 2021 about the new insurance requirements once you cross $10K in sales in a month, that was an INTERNAL policy by Amazon, this new Act if a federal policy under the Federal Trade Commission (FTC), and the FTC is one of the last organizations you want investigating or fining your company.

The penalties for failure to comply with the Act are costly, even for a company the size of Amazon.

The Act authorizes the Federal Trade Commission (FTC) to assess penalties of $46,517 per violation (i.e., for each failure of an online marketplace to collect, verify, or disclose required information). Also, it permits state attorneys general to bring civil actions for violations of the Act.

What does this mean to you as a seller?

Don’t expect to receive several emails for a 30-day extension like you have for those who still need to get insurance (although we expect that to change in September).

The INFORM Consumer Act serves as a robust response to several burgeoning online issues: deceptive practices, counterfeit products, and unauthorized sellers. These problems are at the core of Amazon’s re-verification process, which seeks to eradicate these practices and create a safer shopping environment.

By dovetailing with the stipulations of the INFORM Consumer Act, Amazon hopes to bolster consumer confidence and provide a secure online shopping experience.

Amazon’s reverification process is a critical security feature that confirms the authenticity of its sellers and their offerings. It requires sellers to present relevant documentation that verifies their identity and substantiates the legitimacy of their operations.

This process is a shield for both buyers and sellers against fraudulent activities, reinforcing Amazon as a trustworthy and reliable online marketplace. Amazon’s re-verification process has been frustrating to many sellers who have gone through the re-verification process, only needing to start over. Here is Amazon’s explanation as to why this is happening:

“We acknowledge there have been hiccups in the Amazon reverification process and the subsequent messages relayed, which are part of the problem. We understand the inconvenience this may have caused and extend our apologies,”

Amazon stated in response to recent issues. “If you have already confirmed your re-verification was successful, rest assured, you’re in the clear. We have alerted our seller verification team about the issue, and they are working on a solution. Please stay tuned for updates and relevant information regarding this matter.”

But what happens if you don’t comply with Amazon’s request for information?

Amazon has clarified: “Should we reach out to you with a verification request, we will provide specific instructions and a timeline for response. Failure to respond within the given timeline could, due to legal requirements, lead us to withhold your payments or deactivate your selling account until we receive the necessary information for successful verification.”

Wyoming LLC Requirements for a U.S. Dropshipping Business

Are you looking to form a Wyoming LLC to establish a dropshipping business in the U.S.?

If so, there are many factors to consider, including the legal structure of your business. One popular option for entrepreneurs is forming a limited liability company (LLC) in Wyoming. In this post, we’ll explore the benefits of a Wyoming LLC for your dropshipping business and guide you through the steps to establish a U.S. bank account and obtain a resale certificate.

Benefits of a Wyoming LLC for Your Dropshipping Business

Asset Protection

As a dropshipper, you’re responsible for delivering products to your customers without physically handling inventory. However, you’re still vulnerable to legal issues and liabilities arising from customer complaints, copyright infringements, etc. Forming a Wyoming LLC can provide asset protection by separating your personal assets from those of the business.

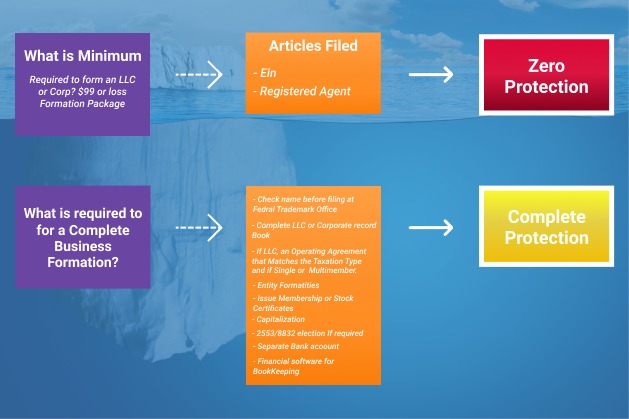

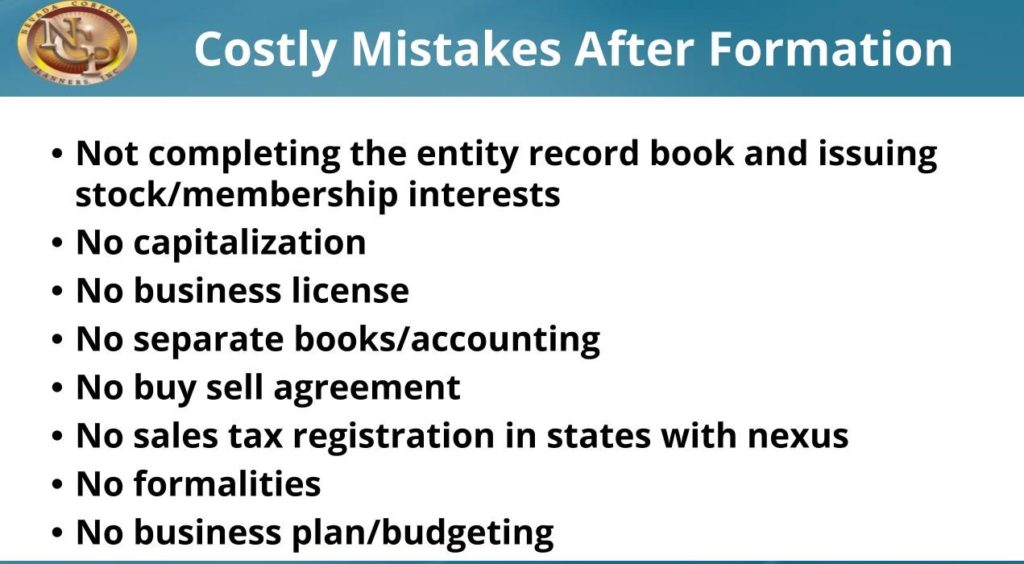

When it comes to forming a Wyoming LLC, it’s crucial to remember that more than simply filing articles of organization is needed to provide legal protection for your business. A shocking 90% of LLCs formed in Wyoming have zero protection because the owners needed to complete formalities beyond the operating agreement.

Just to remind you, an LLC only has protection on the day it’s formed. Afterward, you must operate it as a separate legal entity and avoid commingling funds to ensure continued protection. Adequate capitalization is also critical to maintaining legal protection for your business.

If you don’t take these steps seriously, you could have a personal judgment against you in the U.S., creating severe problems for your business. Even if you can form a new entity, working with suppliers and using A.I. tools for search can still be challenging if your business has a tainted history.

As legal issues arise, proper LLC protection and maintenance is crucial for drop shippers. To help you avoid getting sued, we recommend checking out this informative article from Dodropshipping.com. It covers valuable tips on minimizing the risk of legal issues when dropshipping, including avoiding trademark infringement, using high-quality product images, and providing accurate product descriptions. By following these tips and establishing a solid legal and financial foundation for your dropshipping business, you can reduce your legal risk and focus on confidently growing your business.

Tax Advantages

Wyoming is one of the most business-friendly states in the U.S., with no state income tax, franchise tax, or personal property tax.

While Wyoming may have a sales tax, obtaining a resale certificate can help you save money when working with most U.S. suppliers.

One of the significant benefits of forming a Wyoming LLC is that you’ll only need to file the 5472 and proforma 1120 tax forms, assuming that it’s a single-member LLC disregarded. However, additional or different tax forms may be required if a single-member LLC is taxed as a corporation or a multiple-member LLC is taxed as a partnership.

U.S. taxation can be a complex issue, and it’s essential to understand the requirements to ensure compliance. At this link, you will see the factors involved to evaluate to determine your U.S. tax responsibilities and help you understand your obligations as a business owner. For more information on U.S. taxation requirements, please visit the link on our website.

Forming a single-member LLC in Wyoming is a cost-effective option for non-residents. If they formed a Wyoming LLC, U.S. residents would need to foreign qualify into their home state.

Privacy

Wyoming LLCs offer privacy protection by not requiring owners to disclose their names on public records. Your personal information, including your name and address, will be confidential. The critical question to ask, if privacy is important, is when do I lose my privacy after my LLC formation?

Steps to Establish a U.S. Bank Account and Obtain a Resale CertificateChoose a Business Name and Register Your Wyoming LLC

The first step to establishing your dropshipping business is to choose a business name and register your Wyoming LLC.

If you’re considering forming a Wyoming LLC, you should start with a comprehensive strategy. Don’t make the mistake of simply filing your articles without considering the management structure of your LLC, foreign ownership, and your U.S. tax responsibilities at both the state and federal levels.

To ensure that your business is set up for success, we recommend you conduct a federal trademark search, at a minimum, using the trademark office database. However, for the best results, a comprehensive search is highly recommended. This step can help you avoid costly legal issues and protect your business’s intellectual property.

Apply for an EIN

An EIN (Employer Identification Number) is a unique identifier your business will use when filing taxes and opening a bank account. The key is to complete the SS4 property, which will let the IRS know which U.S. tax returns you plan to file. The SS4 can NOT be amended, so complete it carefully. The SS4 must be faxed to the IRS for non-residents, which may take up to 30 business days. The time frame is also essential for U.S. banking, as they will need the IRS letter with the EIN.

Open a U.S. Bank Account

Once you have your EIN, you can open a U.S. bank account for your Wyoming LLC. You’ll need to provide your EIN, articles of organization, and other identifying information to the bank.

Choosing the right bank is critical when establishing a U.S. bank account for your non-U.S. dropshipping business. Finding a bank familiar with working with non-U.S. residents is essential to ensure a smooth and efficient process.

However, be prepared to provide a personal utility bill in your name that matches your personal address. Most banks typically require this documentation, even if you plan to travel to the U.S. after the pandemic.

Unfortunately, establishing a U.S. bank account for a legal entity (not the individual) can be nearly impossible for non-residents.

Many banks require a personal utility bill in the U.S. linked to your personal address, separate from the documentation required for the LLC formation. If you plan to travel to the U.S., you will likely need help establishing a U.S. bank account.

Be sure to choose a bank familiar with working with non-US residents. Most banks will also want a utility bill in your personal name that matches the same address as your personal address. Even if you plan to travel to the U.S. after the pandemic, establishing a U.S. bank account for a legal entity (not the individual) is almost impossible for non-residents.

Why?

The banks request a personal utility bill in the U.S. linked to your personal address, separate from what they require for the LLC formed.

Obtain a Resale Certificate

A resale certificate lets your business purchase products from suppliers without paying sales tax. To obtain a resale certificate, you must register with your state’s tax authority and provide your EIN and other business information.

A Wyoming resale certificate will suffice in many cases, allowing you to avoid paying sales tax on your purchases. However, it’s important to note that suppliers may require a resale certificate from that specific state in some states, such as nine.

In addition to registering your Wyoming LLC, obtaining a U.S. bank account, and obtaining a resale certificate, there are a few other steps to establish a solid legal and financial foundation for your dropshipping business.

Set Up a U.S. Business Address and Phone Number

You must establish a U.S. business address and phone number to build trust with your suppliers and customers. Without this, you may struggle to communicate effectively and establish credibility in the marketplace.

You can work with a reliable mail forwarding service or virtual office provider to obtain a virtual business address and phone number.

However, it’s essential to ensure that your virtual address is fully compliant and that you have a lease agreement to avoid legal issues.

Also, you should be able to partner with a team that understands the critical items that will be mailed to your virtual address, including verification codes, bank requirements, sales tax permits, and IRS notices.

Set Up a Payment Gateway Account

You must set up a payment gateway account, such as Stripe or PayPal, to accept customer payments. A VPN is a consideration for non-residents regarding these accounts. These gateways allow you to securely process credit card transactions and manage your customers’ payment information. Please choose a payment gateway compatible with your dropshipping platform that offers competitive rates. The key is knowing the entire process, including what happens when an SSN is unavailable.

BE-13 Government Filing

According to a Form BE-13 filing (Survey of New Foreign Direct Investment in the United States), foreign investors in certain U.S. businesses must report their investments. U.S. companies with more than 10% foreign ownership must file a Form BE-13 with the U.S. Bureau of Economic Analysis (BEA), a U.S. Department of Commerce division.

The BE-13 is a complex form due within 45 days of filing your entity. Failure to comply may result in fines of up to $25K, and the BEA may seek injunctive relief. Furthermore, willful violations may result in criminal penalties of up to $10K and imprisonment of up to one year.

Please note that the BE-13 is NOT the same as the 5472 and Proforma 1120, which are federal tax returns related to an SM LLC DE.

For your convenience, we’ve included a link to the BE-13 FAQ page: https://www.bea.gov/help/faq (note that there are 40 tabs of FAQs).

Schedule Your Discovery Call Today

At Nvinc.com, we understand the importance of proper LLC formalities and can help guide you through the process to ensure your business is fully protected. Schedule a discovery call with us today to learn how we can help you establish a solid legal and financial foundation for your dropshipping business. Don’t leave your business vulnerable to legal issues – take action now to protect your future success.

Forming a Wyoming LLC can be an intelligent choice for your dropshipping business, providing asset protection, tax advantages, and privacy. If you’re ready to get started, our team can help guide you through the process.

Schedule your discovery call today at our calendar at this link to learn more about how we can help you launch your U.S. dropshipping business.

Silicon Valley Bank Alternative for Non-U.S. Residents

You will need this Silicon Valley & First Republic Bank alternative as a non-resident business owner. We have important news if you’ve formed a Delaware corporation or U.S. company with Silicon Valley Bank as your only banking partner.

Due to recent regulatory actions by California authorities, Silicon Valley Bank has been closed. On March 10th, Silicon Valley Bank’s assets were seized by FDIC in the most significant bank failure since 2008. Just before noon on the East Coast, the Federal Deposit Insurance Corporation said it was closing the bank. On May 1st, JP Morgan Chase takes over First Republic Bank.

In business, the number one can be your worst enemy. Depending on a single joint venture partner, relying on a solitary source for leads, or working with only one supplier or vendor can leave you vulnerable to a single point of failure. But perhaps the most crucial area where you should avoid being a “one” is banking. Having just ONE BANK ACCOUNT can be a recipe for disaster.

If that account is closed, frozen, or otherwise inaccessible, your business could be brought to its knees. That’s why it’s crucial to diversify your banking relationships and work with multiple partners. Doing so will ensure your funds are protected, and your business can continue operating even if one bank account is compromised. So, if you rely on just one bank account, it’s time to diversify. Don’t let the worst number in business bring you down – instead, take control of your financial future by working with multiple banking partners.

You must find an alternative U.S. bank account to continue operating your business. Fortunately, our team is here to help. We specialize in assisting non-resident business owners like you to set up an alternative banking solution quickly and efficiently.

If you still need a U.S. company formation, first gain clarity on your best U.S. banking options BEFORE forming a U.S. entity. You want to avoid what so many do: to find a low-priced option only to form the LLC and realize either during the process or after opening a U.S. bank account (even without travel) is impossible.

At NCP, our experience since 1997, with thousands of companies formed and working with dozens of banks, brokerage accounts, and online banking platforms.

We have the experience to help you fit all the puzzle pieces in the correct sequence to help you accomplish this task. As we can’t control the banks and their policy changes, we can control how best to form your U.S. company to lead to your best option to establish the bank account. This may involve how the LLC is formed and managed, to a lease agreement without an expensive lease, to match documents and state records to streamline the experience.

Most important is our relationships with our bankers and that we do things right and attract successful entrepreneurs that the banks prefer to work with over time. Let us share our current U.S. banking options and recommendations for 2023.

If you or someone you know needs support, we can help set up your U.S. entity correctly and have all the resources from sales tax to tax returns.

Before we get to the banking details, you must know this ONLY works on a U.S. entity, not a foreign entity.

As you know, we do a lot of work in the e-commerce space, and there are “banking” accounts, such as Payoneer and others.

The challenge is that moving money from one currency to another is great, but they must be fully functioning bank accounts. They do not allow for an ACH pull, which is required to automate the payment of sales taxes.

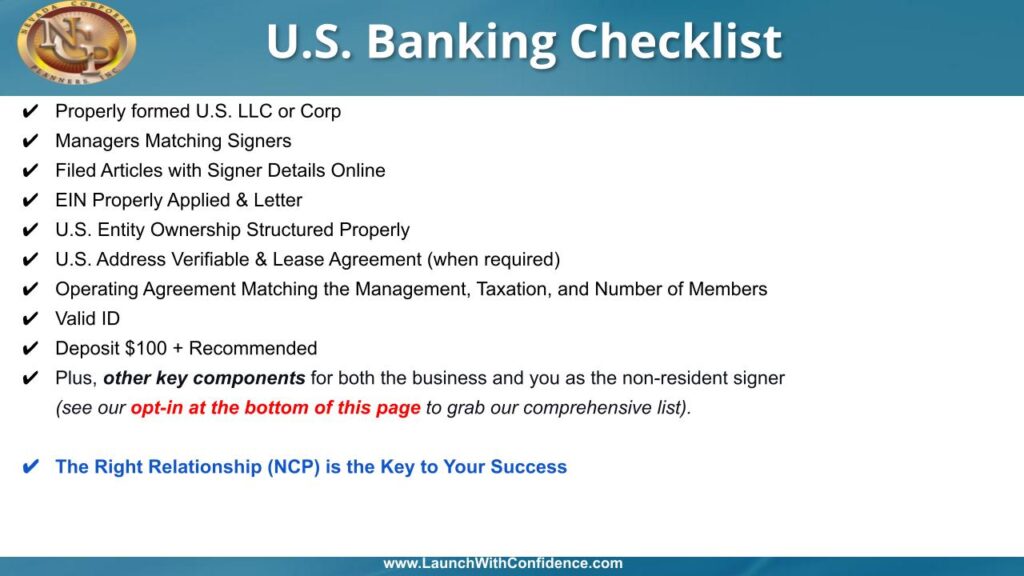

NCP’s U.S. Banking Checklist

We have a relationship with a trustworthy company with a banking platform that works with a bank (not in California) that will work for non-U.S. residents, and you do NOT need to go to the bank in person.

Do you have these questions on your mind?

Is there a monthly bank fee?

We’ve been getting some questions about our banking partner and wanted to clarify some things. First, we want to assure you that our partner does not charge a fee for setting up your account. While we have a fee for the process and introduction, it’s not an extra fee you’ll be charged – it’s simply our fee for facilitating the process.

It’s also important to note that no requirements above and beyond the norm would make it impossible to open an account.

However, some U.S. banks have specific requirements that can cause issues for non-residents. For example, some banks may require a personal utility bill from a U.S. residential address, not a P.O. box, even if you visit the bank in person. Other banks may want to do an official site inspection and see your employees working.

But don’t worry – we’ve got you covered! We’ve compiled a complete checklist for our banking relationship that includes all the information you need to know to ensure a smooth account opening process. You can find it at the bottom of this page.

What is required to open this NEW U.S. Bank Account without Travel:

It is required to have a U.S. entity with an EIN.

You must have a letter from the IRS with your EIN. OurU.S. entity packages include our virtual address service so that the IRS mail will come to our office, and we will scan your IRS letter to your secure folder and your other documents to establish your U.S. bank account. Caution: Avoid banking alternatives that avoid this important compliance step. More compliance is coming, don’t impact your business with shortcuts.

Verify your phone number (from your home country if foreign clients)

ID and selfie verification- a link will be sent to the signer’s phone number to access a page to upload ID and take a selfie verification.

I am setting up multi-factor authentication for logging in to the account.

U.S. address (our virtual address, which is included in our U.S. packages, qualifies)

Ownership structure

Corporation

EIN Verification Letter

Articles of Incorporation/Certificate of Formation/Certificate of Incorporation

Company By-Laws

Government-issued photo I.D. (Passport in color)

U.S. address (our virtual address, which is included in our U.S. packages, qualifies)

Ownership structure

Are you a company owner with a stake in a U.S. entity? If that entity is owned by a company with over 25% ownership, we’ll need the personal information and passports of the beneficial owners who have 25% or more ownership in that company. It’s essential to provide this information to ensure a smooth process.

Don’t stress; we’ve got you covered. We’ve created a comprehensive Silicon Valley Bank alternative checklist to answer all your questions and provide an alternative to Silicon Valley Bank. Our checklist ensures you cover all the bases and get the best service possible. So why wait? Get your hands on our checklist now at this link.

5472 and Proforma 1120 for a U.S. Single-Member LLC Disregarded Owned by a Non-Resident

As a non-U.S. resident with a U.S. single-member LLC, staying compliant with tax laws is crucial. Whether for Amazon Insurance, Shopify payments, or bulk purchases from a U.S. manufacturer, IRS forms 5472 and proforma 1120 for your U.S. single-member LLC disregarded likely must be filed annually.

LLC may require filing Form 5472 and proforma 1120 annually. These forms will come into play the following year after you form your U.S. single-member LLC and obtain an EIN through the IRS. It is important to note how your SS4 was completed, especially for line 9a.

Form 5472 is an information return of a 25% foreign-owned U.S. corporation or a foreign corporation engaged in a U.S. trade or business under sections 6038A and 6038C of the internal revenue code.

It’s important to note that the taxation of a U.S. LLC can vary based on its structure, with single-member LLCs taxed as C corporations requiring both Forms 5472 and 1120. On the other hand, non-resident members of an LLC taxed as a partnership must file IRS Forms 1065, 8804, and 8805.

A failure to timely file a Form 5472 is subject to a $25,000 penalty per information return, plus an additional $25,000 for each month the failure continues, beginning 90 days after the IRS notifies the taxpayer of the failure, with no maximum penalty.

What is new on the instructions for 5472 in 2023?

Part VII lines 41a through 41d. On Form 5472, these lines have been reworded to reflect the final regulations under section 250 (T.D. 9901, 85 FR 43042, July 15, 2020, as amended by 85 FR 68249, Oct. 28, 2020; T.D. 9956, 86 FR 52971, Sept. 24, 2021).

Part VIII lines 48b and 48c. These instructions require a new attachment for Part VIII, lines 48b and 48c. Specifically, if the taxpayer made the election described in Regulations section 1.482-7(d)(3)(iii)(B) or Notice 2005-99, the taxpayer is required to attach the statement described in the instructions for Part VIII, lines 48b and 48c, later.

You would use form 5472 when reportable transactions occur during the tax year of a reporting corporation with a foreign or domestic related party.

What is a Reporting Corporation?A reporting corporation is either:

A 25% foreign-owned U.S. corporation (including a foreign-owned U.S. disregarded entity (DE), or

A foreign corporation engaged in a trade or business within the United States.

Reportable transaction. A reportable transaction includes:

Any transaction listed in Part IV (for example, sales, rents, etc.) for which monetary consideration (including U.S. and foreign currency) was the sole consideration paid or received during the reporting corporation’s tax year;

Any transaction listed in Part V; or

Any transaction or group of transactions listed in Part VI.

However, transactions with a U.S.-related party are not required to be identified explicitly in Parts IV, V, and VI.

Exceptions from filing. A reporting corporation must not file Form 5472 if any of the following apply.

It had no reportable transactions of the types listed in Parts IV and VI of the form and, in the case of a reporting corporation that is a foreign-owned U.S. DE, also had no reportable transactions of the type listed in Part V of the form.

A U.S. person that controls the foreign-related corporation files Form 5471 for the tax year to report information under section 6038. To qualify for this exception, the U.S. person must complete Schedule M (Form 5471) showing all reportable transactions between the reporting corporation and the related party for the tax year. This exception does not apply to foreign-owned U.S. D.E.s.

The related corporation qualifies as a foreign sales corporation for the tax year and files Form 1120-FSC. This exception does not apply to foreign-owned U.S. DEs.

It is a foreign corporation that does not have a permanent establishment in the United States under an applicable income tax treaty and timely files Form 8833.